Optimizing mining operations¶

This tutorial includes everything you need to set up IBM Decision Optimization CPLEX Modeling for Python (DOcplex), build a Mathematical Programming model, and get its solution by solving the model on Cloud with IBM ILOG CPLEX Optimizer.

When you finish this tutorial, you’ll have a foundational knowledge of Prescriptive Analytics.

This notebook is part of Prescriptive Analytics for Python.

It requires a valid subscription to Decision Optimization on Cloud. Try it for free here.

Table of contents:

- Describe the business problem

- How decision optimization can help

- Use decision optimization

- Summary

Describe the business problem¶

This mining operations optimization problem is an implementation of Problem 7 from “Model Building in Mathematical Programming” by H.P. Williams. The operational decisions that need to be made are which mines should be operated each year and how much each mine should produce.

Business constraints¶

- A mine that is closed cannot be worked.

- Once closed, a mine stays closed until the end of the horizon.

- Each year, a maximum number of mines can be worked.

- For each mine and year, the quantity extracted is limited by the mine’s maximum extracted quantity.

- The average blend quality must be greater than or equal to the requirement of the year.

Objective and KPIs¶

Total actualized revenue¶

Each year, the total revenue is equal to the total quantity extracted multiplied by the blend price. The time series of revenues is aggregated in one expected revenue by applying the discount rate; in other terms, a revenue of $1000 next year is counted as $900 actualized, $810 if the revenue is expected in two years, etc.

Total expected royalties¶

A mine that stays open must pay royalties (see the column royalties in the DataFrame). Again, royalties from different years are actualized using the discount rate.

Business objective¶

The business objective is to maximize the net actualized profit, that is the difference between the total actualized revenue and total actualized royalties.

How decision optimization can help¶

Prescriptive analytics (decision optimization) technology recommends actions that are based on desired outcomes. It takes into account specific scenarios, resources, and knowledge of past and current events. With this insight, your organization can make better decisions and have greater control of business outcomes.

Prescriptive analytics is the next step on the path to insight-based actions. It creates value through synergy with predictive analytics, which analyzes data to predict future outcomes.

- Prescriptive analytics takes that insight to the next level by suggesting the optimal way to handle that future situation. Organizations that can act fast in dynamic conditions and make superior decisions in uncertain environments gain a strong competitive advantage.

With prescriptive analytics, you can:

- Automate the complex decisions and trade-offs to better manage your limited resources.

- Take advantage of a future opportunity or mitigate a future risk.

- Proactively update recommendations based on changing events.

- Meet operational goals, increase customer loyalty, prevent threats and fraud, and optimize business processes.

Checking minimum requirements¶

This notebook uses some features of pandas that are available in version 0.17.1 or above.

import pip

REQUIRED_MINIMUM_PANDAS_VERSION = '0.17.1'

d = {pkg.key : pkg.version for pkg in pip.get_installed_distributions()}

try:

assert d['pandas'] >= REQUIRED_MINIMUM_PANDAS_VERSION

except:

raise Exception("Version " + REQUIRED_MINIMUM_PANDAS_VERSION + " or above of Pandas is required to run this notebook")

Use decision optimization¶

Step 1: Download the library¶

Run the following code to install the Decision Optimization CPLEX Modeling library. The DOcplex library contains the two modeling packages, Mathematical Programming and Constraint Programming, referred to earlier.

import sys

try:

import docplex.mp

except:

if hasattr(sys, 'real_prefix'):

#we are in a virtual env.

!pip install docplex

else:

!pip install --user docplex

Note that the more global package docplex contains another subpackage docplex.cp that is dedicated to Constraint Programming, another branch of optimization.

Step 2: Set up the prescriptive engine¶

- Subscribe to the Decision Optimization on Cloud solve service.

- Get the service URL and your personal API key and enter your credentials here:

url = "ENTER YOUR URL HERE"

key = "ENTER YOUR KEY HERE"

Step 3: Model the data¶

Mining Data¶

The mine data is provided as a pandas DataFrame. For each mine, we are given the amount of royalty to pay when operating the mine, its ore quality, and the maximum quantity that we can extract from the mine.

# If needed, install the module pandas prior to executing this cell

import pandas as pd

from pandas import DataFrame, Series

df_mines = DataFrame({"royalties": [ 5 , 4, 4, 5 ],

"ore_quality": [ 1.0, 0.7, 1.5, 0.5],

"max_extract": [ 2 , 2.5, 1.3, 3 ]})

nb_mines = len(df_mines)

df_mines.index.name='range_mines'

df_mines

| max_extract | ore_quality | royalties | |

|---|---|---|---|

| range_mines | |||

| 0 | 2.0 | 1.0 | 5 |

| 1 | 2.5 | 0.7 | 4 |

| 2 | 1.3 | 1.5 | 4 |

| 3 | 3.0 | 0.5 | 5 |

Blend quality data¶

Each year, the average blend quality of all ore extracted from the mines must be greater than a minimum quality. This data is provided as a pandas Series, the length of which is the plan horizon in years.

blend_qualities = Series([0.9, 0.8, 1.2, 0.6, 1.0])

nb_years = len(blend_qualities)

print("* Planning mining operations for: {} years".format(nb_years))

blend_qualities.describe()

* Planning mining operations for: 5 years

count 5.000000

mean 0.900000

std 0.223607

min 0.600000

25% 0.800000

50% 0.900000

75% 1.000000

max 1.200000

dtype: float64

Additional (global) data¶

We need extra global data to run our planning model:

- a blend price (supposedly flat),

- a maximum number of worked mines for any given years (typically 3), and

- a discount rate to compute the actualized revenue over the horizon.

# global data

blend_price = 10

max_worked_mines = 3 # work no more than 3 mines each year

discount_rate = 0.10 # 10% interest rate each year

Step 4: Prepare the data¶

The data is clean and does not need any cleansing.

Step 5: Set up the prescriptive model¶

from docplex.mp.environment import Environment

env = Environment()

env.print_information()

* system is: Windows 64bit

* Python is present, version is 2.7.11

* docplex is present, version is (1, 0, 0)

Create DOcplex model¶

The model contains all the business constraints and defines the objective.

from docplex.mp.model import Model

mm = Model("mining_pandas")

What are the decisions we need to make?

- What mines do we work each year? (a yes/no decision)

- What mine do we keep open each year? (again a yes/no decision)

- What quantity is extracted from each mine, each year? (a positive number)

We need to define some decision variables and add constraints to our model related to these decisions.

Define the decision variables¶

# auxiliary data: ranges

range_mines = range(nb_mines)

range_years = range(nb_years)

# binary decisions: work the mine or not

work_vars = mm.binary_var_matrix(keys1=range_mines, keys2=range_years, name='work')

# open the mine or not

open_vars = mm.binary_var_matrix(range_mines, range_years, name='open')

# quantity to extract

ore_vars = mm.continuous_var_matrix(range_mines, range_years, name='ore')

mm.print_information()

Model: mining_pandas

- number of variables: 60

- binary=40, integer=0, continuous=20

- number of constraints: 0

- LE=0, EQ=0, GE=0, RNG=0

- parameters: defaults

Express the business constraints¶

Constraint 1: Only open mines can be worked.¶

In order to take advantage of the pandas operations to create the optimization model, decision variables are organized in a DataFrame which is automatically indexed by ‘range_mines’ and ‘range_years’ (that is, the same keys as the dictionary created by the binary_var_matrix() method).

# Organize all decision variables in a DataFrame indexed by 'range_mines' and 'range_years'

df_decision_vars = DataFrame({'work': work_vars, 'open': open_vars, 'ore': ore_vars})

# Set index names

df_decision_vars.index.names=['range_mines', 'range_years']

# Display rows of 'df_decision_vars' DataFrame for first mine

df_decision_vars[:nb_years]

| open | ore | work | ||

|---|---|---|---|---|

| range_mines | range_years | |||

| 0 | 0 | open_0_0 | ore_0_0 | work_0_0 |

| 1 | open_0_1 | ore_0_1 | work_0_1 | |

| 2 | open_0_2 | ore_0_2 | work_0_2 | |

| 3 | open_0_3 | ore_0_3 | work_0_3 | |

| 4 | open_0_4 | ore_0_4 | work_0_4 |

Now, let’s iterate over rows of the DataFrame “df_decision_vars” and enforce the desired constraint.

The pandas method itertuples() returns a named tuple for each row of a DataFrame. This method is efficient and convenient for iterating over all rows.

mm.add_constraints(t.work <= t.open

for t in df_decision_vars.itertuples())

mm.print_information()

Model: mining_pandas

- number of variables: 60

- binary=40, integer=0, continuous=20

- number of constraints: 20

- LE=20, EQ=0, GE=0, RNG=0

- parameters: defaults

Constraint 2: Once closed, a mine stays closed.¶

These constraints are a little more complex: we state that the series of open_vars[m,y] for a given mine m is decreasing. In other terms, once some open_vars[m,y] is zero, all subsequent values for future years are also zero.

Let’s use the pandas groupby operation to collect all “open” decision variables for each mine in separate pandas Series. Then, we iterate over the mines and invoke the aggregate() method, passing the postOpenCloseConstraint() function as the argument. The pandas aggregate() method invokes postOpenCloseConstraint() for each mine, passing the associated Series of “open” decision variables as argument. The postOpenCloseConstraint() function posts a set of constraints on the sequence of “open” decision variables to enforce that a mine cannot re-open.

# Once closed, a mine stays closed

def postOpenCloseConstraint(openDVars):

mm.add_constraints(open_next <= open_curr

for (open_next, open_curr) in zip(openDVars[1:], openDVars))

# Optionally: return a string to display information regarding the aggregate operation in the Output cell

return "posted "+ repr(len(openDVars) - 1) + " constraints"

# Constraints on sequences of decision variables are posted for each mine, using pandas' "groupby" operation.

df_decision_vars.open.groupby(level='range_mines').aggregate(postOpenCloseConstraint)

range_mines

0 posted 4 constraints

1 posted 4 constraints

2 posted 4 constraints

3 posted 4 constraints

Name: open, dtype: object

Constraint 3: The number of worked mines each year is limited.¶

This time, we use the pandas groupby operation to collect all “work” decision variables for each year in separate pandas Series. Each Series contains the “work” decision variables for all mines. Then, the maximum number of worked mines constraint is enforced by making sure that the sum of all the terms of each Series is smaller or equal to the maximum number of worked mines. The aggregate() method is used to post this constraint for each year.

# Maximum number of worked mines each year

df_decision_vars.work.groupby(level='range_years').aggregate(

lambda works: mm.add_constraint(mm.sum(works.values) <= max_worked_mines))

range_years

0 work_0_0+work_1_0+work_2_0+work_3_0 <= 3

1 work_0_1+work_1_1+work_3_1+work_2_1 <= 3

2 work_0_2+work_1_2+work_2_2+work_3_2 <= 3

3 work_0_3+work_1_3+work_3_3+work_2_3 <= 3

4 work_0_4+work_1_4+work_3_4+work_2_4 <= 3

Name: work, dtype: object

Constraint 4: The quantity extracted is limited.¶

This constraint expresses two things: * Only a worked mine can give ore. (Note that there is no minimum on the quantity extracted, this model is very simplified). * The quantity extracted is less than the mine’s maximum extracted quantity.

To illustrate the pandas join operation, let’s build a DataFrame that joins the “df_decision_vars” DataFrame and the “df_mines.max_extract” Series such that each row contains the information to enforce the quantity extracted limit constraint. The default behaviour of the pandas join operation is to look at the index of left DataFrame and to append columns of the right Series or DataFrame which have same index. Here is the result of this operation in our case:

# Display rows of 'df_decision_vars' joined with 'df_mines.max_extract' Series for first two mines

df_decision_vars.join(df_mines.max_extract)[:(nb_years * 2)]

| open | ore | work | max_extract | ||

|---|---|---|---|---|---|

| range_mines | range_years | ||||

| 0 | 0 | open_0_0 | ore_0_0 | work_0_0 | 2.0 |

| 1 | open_0_1 | ore_0_1 | work_0_1 | 2.0 | |

| 2 | open_0_2 | ore_0_2 | work_0_2 | 2.0 | |

| 3 | open_0_3 | ore_0_3 | work_0_3 | 2.0 | |

| 4 | open_0_4 | ore_0_4 | work_0_4 | 2.0 | |

| 1 | 0 | open_1_0 | ore_1_0 | work_1_0 | 2.5 |

| 1 | open_1_1 | ore_1_1 | work_1_1 | 2.5 | |

| 2 | open_1_2 | ore_1_2 | work_1_2 | 2.5 | |

| 3 | open_1_3 | ore_1_3 | work_1_3 | 2.5 | |

| 4 | open_1_4 | ore_1_4 | work_1_4 | 2.5 |

Now, the constraint to limit quantity extracted is easily created by iterating over all rows of the joined DataFrames:

# quantity extracted is limited

mm.add_constraints(t.ore <= t.max_extract * t.work

for t in df_decision_vars.join(df_mines.max_extract).itertuples())

mm.print_information()

Model: mining_pandas

- number of variables: 60

- binary=40, integer=0, continuous=20

- number of constraints: 61

- LE=61, EQ=0, GE=0, RNG=0

- parameters: defaults

Blend constraints¶

We need to compute the total production of each year, stored in auxiliary variables.

Again, we use the pandas groupby operation, this time to collect all “ore” decision variables for each year in separate pandas Series. The “blend” variable for a given year is the sum of “ore” decision variables for the corresponding Series.

# blend variables

blend_vars = mm.continuous_var_list(nb_years, name='blend')

# define blend variables as sum of extracted quantities

mm.add_constraints(mm.sum(ores.values) == blend_vars[year]

for year, ores in df_decision_vars.ore.groupby(level='range_years'))

mm.print_information()

Model: mining_pandas

- number of variables: 65

- binary=40, integer=0, continuous=25

- number of constraints: 66

- LE=61, EQ=5, GE=0, RNG=0

- parameters: defaults

Minimum average blend quality constraint¶

The average quality of the blend is the weighted sum of extracted quantities, divided by the total extracted quantity. Because we cannot use division here, we transform the inequality:

# Quality requirement on blended ore

mm.add_constraints(mm.sum(ores.values * df_mines.ore_quality) >= blend_qualities[year] * blend_vars[year]

for year, ores in df_decision_vars.ore.groupby(level='range_years'))

mm.print_information()

Model: mining_pandas

- number of variables: 65

- binary=40, integer=0, continuous=25

- number of constraints: 71

- LE=61, EQ=5, GE=5, RNG=0

- parameters: defaults

KPIs and objective¶

Since both revenues and royalties are actualized using the same rate, we compute an auxiliary discount rate array.

The discount rate array¶

actualization = 1.0 - discount_rate

assert actualization > 0

assert actualization <= 1

#

s_discounts = Series((actualization ** y for y in range_years), index=range_years, name='discounts')

s_discounts.index.name='range_years'

# e.g. [1, 0.9, 0.81, ... 0.9**y...]

print(s_discounts)

range_years

0 1.0000

1 0.9000

2 0.8100

3 0.7290

4 0.6561

Name: discounts, dtype: float64

Total actualized revenue¶

Total expected revenue is the sum of actualized yearly revenues, computed as total extracted quantities multiplied by the blend price (assumed to be constant over the years in this simplified model).

expected_revenue = blend_price * mm.dot(blend_vars, s_discounts)

mm.add_kpi(expected_revenue, "Total Actualized Revenue")

DecisionKPI(name=Total Actualized Revenue,expr=10blend_0+9blend_1+7.290blend_3+8.100blend_2+6.561blend_4)

Total actualized royalty cost¶

The total actualized royalty cost is computed for all open mines, also actualized using the discounts array.

This time, we use the pandas join operation twice to build a DataFrame that joins the “df_decision_vars” DataFrame with the “df_mines.royalties” and “s_discounts” Series such that each row contains the relevant information to calculate its contribution to the total actualized royalty cost. The join with the “df_mines.royalties” Series is performed by looking at the common “range_mines” index, while the join with the “s_discounts” Series is performed by looking at the common “range_years” index.

df_royalties_data = df_decision_vars.join(df_mines.royalties).join(s_discounts)

df_royalties_data

| open | ore | work | royalties | discounts | ||

|---|---|---|---|---|---|---|

| range_mines | range_years | |||||

| 0 | 0 | open_0_0 | ore_0_0 | work_0_0 | 5 | 1.0000 |

| 1 | open_0_1 | ore_0_1 | work_0_1 | 5 | 0.9000 | |

| 2 | open_0_2 | ore_0_2 | work_0_2 | 5 | 0.8100 | |

| 3 | open_0_3 | ore_0_3 | work_0_3 | 5 | 0.7290 | |

| 4 | open_0_4 | ore_0_4 | work_0_4 | 5 | 0.6561 | |

| 1 | 0 | open_1_0 | ore_1_0 | work_1_0 | 4 | 1.0000 |

| 1 | open_1_1 | ore_1_1 | work_1_1 | 4 | 0.9000 | |

| 2 | open_1_2 | ore_1_2 | work_1_2 | 4 | 0.8100 | |

| 3 | open_1_3 | ore_1_3 | work_1_3 | 4 | 0.7290 | |

| 4 | open_1_4 | ore_1_4 | work_1_4 | 4 | 0.6561 | |

| 2 | 0 | open_2_0 | ore_2_0 | work_2_0 | 4 | 1.0000 |

| 1 | open_2_1 | ore_2_1 | work_2_1 | 4 | 0.9000 | |

| 2 | open_2_2 | ore_2_2 | work_2_2 | 4 | 0.8100 | |

| 3 | open_2_3 | ore_2_3 | work_2_3 | 4 | 0.7290 | |

| 4 | open_2_4 | ore_2_4 | work_2_4 | 4 | 0.6561 | |

| 3 | 0 | open_3_0 | ore_3_0 | work_3_0 | 5 | 1.0000 |

| 1 | open_3_1 | ore_3_1 | work_3_1 | 5 | 0.9000 | |

| 2 | open_3_2 | ore_3_2 | work_3_2 | 5 | 0.8100 | |

| 3 | open_3_3 | ore_3_3 | work_3_3 | 5 | 0.7290 | |

| 4 | open_3_4 | ore_3_4 | work_3_4 | 5 | 0.6561 |

The total royalty is now calculated by multiplying the columns “open”, “royalties” and “discounts”, and to sum over all rows. Using pandas constructs, this can be written in a very compact way as follows:

total_royalties = mm.sum((df_royalties_data.open * df_royalties_data.royalties * df_royalties_data.discounts).values)

mm.add_kpi(total_royalties, "Total Actualized Royalties")

DecisionKPI(name=Total Actualized Royalties,expr=4.050open_0_2+3.600open_1_1+2.916open_1_3+2.916open_2_3+4open_1_0+5open_0_0+4open_2_0+3.240open_2_2+5open_3_0+3.240open_1_2+3.280open_0_4+4.500open_0_1+4.050open_3_2+2.624open_1_4+3.645open_3_3+3.645open_0_3+2.624open_2_4+3.280open_3_4+3.600open_2_1+4.500open_3_1)

Express the objective¶

The business objective is to maximize the expected net profit, which is the difference between revenue and royalties.

mm.maximize(expected_revenue - total_royalties)

Solve with the Decision Optimization solve service¶

Solve the model on the cloud.

mm.print_information()

assert mm.solve(url=url, key=key), "!!! Solve of the model fails"

mm.report()

Model: mining_pandas

- number of variables: 65

- binary=40, integer=0, continuous=25

- number of constraints: 71

- LE=61, EQ=5, GE=5, RNG=0

- parameters: defaults

* model solved with objective: 161.438

* KPI: Total Actualized Revenue=214.674

* KPI: Total Actualized Royalties=53.236

Step 6: Investigate the solution and then run an example analysis¶

To analyze the results, we again leverage pandas, by storing the solution value of the ore variables in a new DataFrame. Note that we use the float function of Python to convert the variable to its solution value. Of course, this requires that the model be successfully solved. For convenience, we want to organize the ore solution values in a pivot table with years as row index and mines as columns. The pandas unstack operation does this for us.

mine_labels = [("mine%d" % (m+1)) for m in range_mines]

ylabels = [("y%d" % (y+1)) for y in range_years]

# Add a column to DataFrame containing 'ore' decision variables value and create a pivot table by (years, mines)

df_decision_vars['ore_values']=map(float, df_decision_vars.ore)

# Create a pivot table by (years, mines), using pandas' "unstack" method to transform the 'range_mines' row index

# into columns

df_res = df_decision_vars.ore_values.unstack(level='range_mines')

# Set user-friendly labels for column and row indices

df_res.columns = mine_labels

df_res.index = ylabels

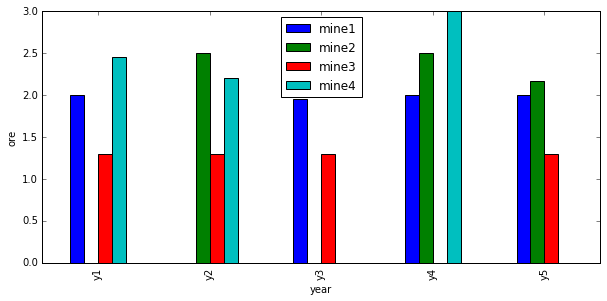

df_res

| mine1 | mine2 | mine3 | mine4 | |

|---|---|---|---|---|

| y1 | 2.00 | 2.500000 | 1.3 | 0.0 |

| y2 | 2.00 | 2.500000 | 1.3 | 0.0 |

| y3 | 1.95 | 0.000000 | 1.3 | 0.0 |

| y4 | 2.00 | 2.500000 | 1.3 | 0.0 |

| y5 | 2.00 | 2.166667 | 1.3 | 0.0 |

import matplotlib.pyplot as plt

%matplotlib inline

df_res.plot(kind="bar", figsize=(10,4.5))

plt.xlabel("year")

plt.ylabel("ore")

<matplotlib.text.Text at 0xac53240>

Adding operational constraints.¶

What if we wish to add operational constraints? For example, let us forbid work on certain pairs of (mines, years). Let’s see how this impacts the profit.

First, we add extra constraints to forbid work on those tuples.

# a list of (mine, year) tuples on which work is not possible.

forced_stops = [(1, 2), (0, 1), (1, 0), (3, 2), (2, 3), (3, 4)]

mm.add_constraints(work_vars[stop_m, stop_y] == 0

for stop_m, stop_y in forced_stops)

mm.print_information()

Model: mining_pandas

- number of variables: 65

- binary=40, integer=0, continuous=25

- number of constraints: 77

- LE=61, EQ=11, GE=5, RNG=0

- parameters: defaults

The previous solution does not satisfy these constraints; for example (0, 1) means mine 1 should not be worked on year 2, but it was in fact worked in the above solution. To help CPLEX find a feasible solution, we will build a heuristic feasible solution and pass it to CPLEX.

Using an heuristic start solution¶

In this section, we show how one can provide a start solution to CPLEX, based on heuristics.

First, we build a solution in which mines are worked whenever possible, that is for all couples (m,y) except for those in forced_stops.

from docplex.mp.solution import SolveSolution

full_mining = SolveSolution(mm)

for m in range_mines:

for y in range_years:

if (m,y) not in forced_stops:

full_mining.add_var_value(work_vars[m,y], 1)

#full_mining.display()

Then we pass this solution to the model as a MIP start solution and re-solve, this time with CPLEX logging turned on.

mm.add_mip_start(full_mining)

s3 = mm.solve(url=url, key=key, log_output=True) # turns on CPLEX logging

assert s3, "solve failed"

mm.report()

2 of 5 MIP starts provided solutions.

MIP start 'm5' defined initial solution with objective 157.9355.

Tried aggregator 5 times.

MIP Presolve eliminated 41 rows and 29 columns.

MIP Presolve modified 29 coefficients.

Aggregator did 36 substitutions.

All rows and columns eliminated.

Presolve time = 0.00 sec. (0.17 ticks)

Root node processing (before b&c):

Real time = 0.02 sec. (0.33 ticks)

Parallel b&c, 8 threads:

Real time = 0.00 sec. (0.00 ticks)

Sync time (average) = 0.00 sec.

Wait time (average) = 0.00 sec.

------------

Total (root+branch&cut) = 0.02 sec. (0.33 ticks)

* model solved with objective: 157.936

* KPI: Total Actualized Revenue=228.367

* KPI: Total Actualized Royalties=70.431

You can see in the CPLEX log above, that our MIP start solution provided a good start for CPLEX, defining an initial solution with objective 157.9355

Now we can again visualize the results with pandas and matplotlib.

# Add a column to DataFrame containing 'ore' decision variables value and create a pivot table by (years, mines)

df_decision_vars['ore_values2']=map(float, df_decision_vars.ore)

df_res2 = df_decision_vars.ore_values2.unstack(level='range_mines')

df_res2.columns = mine_labels

df_res2.index = ylabels

df_res2.plot(kind="bar", figsize=(10,4.5))

plt.xlabel("year")

plt.ylabel("ore")

<matplotlib.text.Text at 0xca93128>

As expected, mine1 is not worked in year 2: there is no blue bar at y2.

Summary¶

You learned how to set up and use IBM Decision Optimization CPLEX Modeling for Python to formulate a Mathematical Programming model and solve it with IBM Decision Optimization on Cloud.

References¶

- CPLEX Modeling for Python documentation

- Decision Optimization on Cloud

- Need help with DOcplex or to report a bug? Please go here.

- Contact us at dofeedback@wwpdl.vnet.ibm.com.